BBRS Quarterly Insight Report – April 2022

25 April 2022

Business Banking Resolution Service (BBRS) Quarterly Insight Report – April 2022

The BBRS is an independent organisation, both in its decision-making and its operations. It was established to help Small and Medium sized business Enterprises (SMEs) who have not had access to other forms of dispute resolution.

The organisation’s key goal remains to resolve disputes fairly between businesses and banks; and to promote trust in business banking relationships. The BBRS has been working towards this goal by adjudicating cases impartially, based on what is fair and reasonable, using Alternative Dispute Resolutions practices.

This is the fourth BBRS Quarterly Insights Report, providing information about our casework between the BBRS launching on 15 February 2021 through to 31 March 2022.

February 2022 marked a year since the BBRS was launched. Customers have continued to be at the heart of what we do, and the BBRS remains focused on delivering an excellent customer experience.

Registrations

As of 31 March 2022, the BBRS had a total of 776 registered cases. Of these, 59% were historical cases (relating to complaints between 2001 and 2019), 16% were contemporary cases (relating to complaints since 2019) and 25% had not yet been established as either historical or contemporary due to insufficient preliminary customer data.

When the BBRS launched in February 2021, the number of cases was heavily weighted towards the historical scheme. This was due to the existing awareness of the BBRS among SME groups that were involved in the set-up of the BBRS. Since then, the number of historic cases has fallen whilst the number of contemporary cases has increased. This trend is as expected, as awareness of the service grows.

The number of historic cases being registered may increase, going forward, as the BBRS launches an awareness campaign to encourage complainants under the historical scheme before this scheme closes to new complaints on 14 February 2023.

| Total | Percentage | |

| Historic | 457 | 59% |

| Contemporary | 123 | 16% |

| Unestablished date of complaint | 196 | 25% |

| Total | 776 |

The total number of cases registered with the BBRS.

Case Status

As of 31 March 2022, the BBRS had 161 open cases and 615 closed cases.

Of the 776 cases that have come to the BBRS, 526 were closed for reasons not related to ineligibility. This could have included, for example, the removal of duplicate cases, customers withdrawing their complaint from the process or closure due to prolonged customer inaction.

Cases that were closed due to prolonged customer inaction were de-registered. These cases had not generally been the subject of a formal Eligibility Assessment, and these customers can re-register in the future if they wish to do so. Cases were only de-registered following sustained and unsuccessful efforts to communicate with the customer.

There were no open cases waiting for a customer champion to be allocated.

| Total | Percentage | |

| To be allocated | 0 | 0% |

| Live | 161 | 21% |

| Closed | 615 | 79% |

| Total | 776 |

Eligibility

The BBRS treats all cases as eligible until it establishes the facts relating to each complaint. When a complaint is first assembled, information is collected to check eligibility.

When there is a clear early challenge or lack of clarity, the customer is made aware as soon as possible. Not all cases require or receive a formal Eligibility Assessment. All cases are continuously evaluated during case assembly by the allocated customer champion and the Case Assessor, and only those cases where there is uncertainty regarding eligibility undergo a formal Eligibility Assessment by a Case Assessor.

After a case has received a formal Eligibility Assessment from a Case Assessor, the case may be subject to appeal by either party.

As of 31 March 2022, of the open cases, 137 were progressing as being eligible for the BBRS compared to 24 cases that had been assessed as ineligible, although this number could reduce subject to appeal. Of the closed cases, 89 were found to be ineligible.

The eligibility of every case is kept under review throughout the entire complaint journey – as a result most cases will fall into the ‘open cases progressing as eligible’ category until they require an Eligibility Assessment or receive a Provisional Determination.

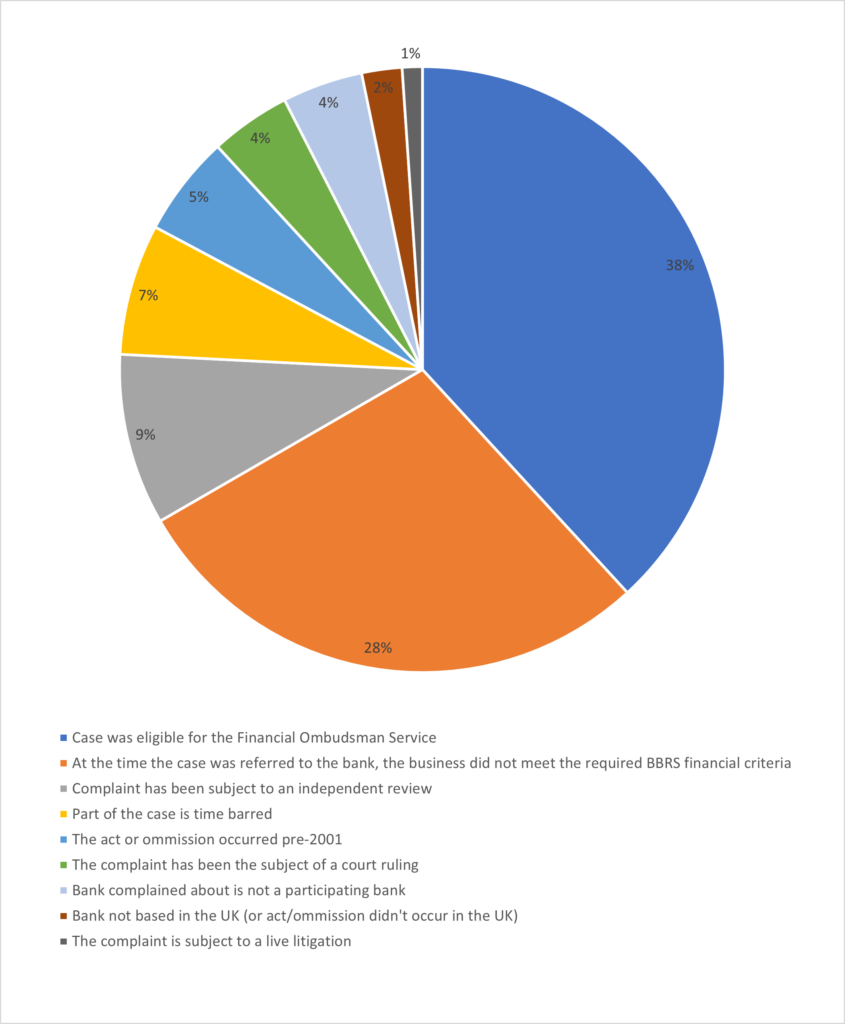

Reasons for Ineligibility

The chart below shows the total number of reasons why cases were found ineligible for the BBRS following formal Eligibility Assessments.

The most common reason for ineligibility remains that a case was currently, or was previously, eligible for – or received an outcome from – the Financial Ombudsman Service.

The second most common reason was at the time the customers complaint was referred to the bank, the business appeared not to meet the required BBRS financial criteria.

There can be one or more reasons affecting eligibility per case. As of 31 March 2022, 41% of ineligible cases had multiple reasons making them ineligible for consideration.

Concessionary Cases

If a case falls outside the BBRS’ eligibility criteria, the BBRS may still be able to consider it provided the customer, the bank and the BBRS all agree. If we are asked to consider a complaint and we believe we should be able to do so (for example because there is a technical reason why it is ineligible or it has just fallen short of our eligibility criteria), we will write to the bank, explain why we think we should consider it, and we will ask for the bank’s agreement.

The BBRS considered the option of the concessionary case process in all cases which were found ineligible following an Eligibility Assessment.

As of 31 March 2022, the BBRS had referred 26 cases to banks for the concessionary case process. Of these, seven cases were taken forward and 16 were not progressed. Three were referred to other ADR Schemes.

Eligibility Appeals

The BBRS recognises that there may still be some situations when either party feels there is more to be considered about the case and wish to appeal part of, or the whole, Eligibility Assessment, after it is issued.

Permissible grounds of appeal are:

- Mistakes: If there has been a clear error of fact or law in the decision being appealed

- New information: If there is new evidence or information relating to the decision that has only become available since the decision was issued

- Non-compliance with Scheme Rules: If the BBRS, in handling the case, has failed to comply with the Scheme Rules in a material way and this has had a material impact on the outcome.

As of 31 March 2022, the BBRS had received 41 appeals notices in relation to Eligibility Assessments. This is from a total of 113 Eligibility Assessments which had been undertaken to date.

This number was higher than the organisation originally anticipated. Many cases were registered before the Scheme Rules were agreed and published, and the BBRS went live.

Of the 41 appeal notices that have been received so far:

- An appeals panel is considering five appeal notices

- 27 appeals had been unsuccessful as they did not meet the grounds required

- Nine appeals have not been upheld and did not proceed to adjudication.

Determinations

Both parties to a complaint can respond to a Provisional Determination after it is issued. Any responses to the Provisional Determination are considered before the issuing of the Determination.

There have so far been 11 Determinations, with a range of outcomes.

The BBRS only reports on closed cases in terms of outcomes. As of 31 March 2022, eight cases had closed. Of these one was upheld in full, six were partially upheld and one was not upheld.

Of the eight closed cases, six were awarded financial awards and two received non-financial awards. These figures include any financial awards issued for Distress and Inconvenience, regardless of whether the complaint was substantively upheld.

Conclusion

The BBRS continues to see customers registering cases for the service, with a more balanced split between historical and contemporary cases. This is expected to continue into the remainder of 2022.

Where a case has been found to be ineligible through formal assessment, eligibility for the Financial Ombudsman Services remains the most common reason. A fundamental principle has long been that the jurisdiction of the BBRS cannot overlap with the jurisdiction of the Financial Ombudsman Service because it is a statutory body.

Not reflected in the figures in this report is the number of cases going through alternative means of resolving disputes. Since its launch, the BBRS has seen levels of trust in alternative dispute resolution from both banks and customers increasing.

As at 31 March 2022 15 cases had moved from the adjudication process and into alternative dispute resolution (ADR). Several cases had either received settlement offers from the responding bank, or were in conciliated settlement, or were taking part in mediation.